Today's China is one of the Internet's hottest industry finance. Changers BAT already mouthwatering koth, rewarding P2P platforms, such as the spoiler into the no man's land, and changing the traditional banks and traditional financial institutions after the cold water was poured over a face felt, found her site has long been riddled with problems.

This protracted war the human, material and financial resources invested, far more than other Internet money invested in world war.

Across the United States, can bring this war which "weathervane"?

Why did China not Lending Club?

When people were laughing at United States no "Internet banking" when United States of P2P companies Lending Club (hereinafter referred to as LC) were already on the market. Was founded in October 2006 by LC first just a Facebook application, and later into person-to-person microfinance platform independent development. In December 2014, LC successfully listed its shares on the New York Stock Exchange, could fetch more than $ 9 billion.

Many well-known Internet companies are copying the United States model, but LC is not necessarily suitable for "Copy to China", it has many different practices and Chinese P2P platform.

In addition to established, populations, socio-cultural environment different than LC and the demands faced by Chinese P2P platform are also very different. Appropriate credit CEO Fang Yihan Xinyi people tell Tencent technology, LC platform of borrowers in the United States other credit agency also can borrow money, borrowers chose LC in order to save money. P2P platform in China, can I borrow the money issues of most concern is the borrower. LC's brand slogan is "better interest rates", while several P2P platform's slogan has "borrowed" words.

In addition, the United States has a very powerful FICO (Fei Aizhe) credit scoring system, complete and effective personal credit information is included, not only the United States of the three major credit Bureau will adopt its report, even the big banks this is a personal loan and how much to loan basis.

In the United States as long as you have a SSN (social security number), from small to big personal credit situation at a glance. It not only can be used for filing tax returns, even applying for driver's licenses, open bank accounts, apartment rental can be used. Therefore, LC was the basis for the personal loan, borrowers can be done online, no longer need to authenticate offline. The Internet times new raise pattern

But in China, because there is no similar credit scoring system, online cannot accurately determine the authenticity of the identity of the borrower as well as on the repayment ability of most platforms only to line gets the borrower.

Enabling network cooperate with FICO as early as in early 2013, the latter's technology risk management. Pat loan learned LC mode, only the online person-to-person lending.

Pat credit CEO Zhang told Tencent technology, Pat credit of its own control system released in March this year, "magic mirror", the system will take into account the borrower's information, even microblog and QQ space, and so on, for each loan to a relative risk rating.

However, even so, because of the lack of data, enabling network and Pat loan, credit assessment in the future for a long period of time will also be a major unanswered problems.

United States really doesn't "Internet banking"?

Internet finance in China while fighting was going on, people are surprised to find, across the United States there is no so-called "Internet banking". Then quickly jump to assert: the Internet finance in China is better. However, the facts really true? We may wish to compare Internet financial companies in China and overseas.

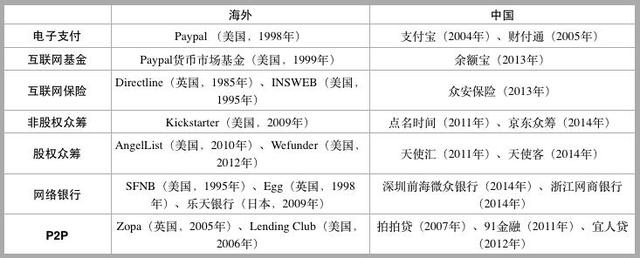

According to statistics from Tencent technology, United States in all areas of Internet financial started early in China, and the vast majority are leading in the field for more than 5 years. The various modes of Internet finance in China, also in the United States found the prototype.

The American version of "balance of treasure" Paypal money market fund, for example, as early as in 1999, the product has been born, stumbled. In 2007, the Fund yields have climbed to 5.1%, capital accumulation has reached its peak. But after the financial crisis of 2008, United States implementation of the zero interest rate policy that all money Fund yields are very low, Paypal money market fund yield "green" has gradually shrunk the size. Finally, in 2011, Paypal option to turn it off. But when it come to an end, across the ocean in balance treasure are not yet available.

Raised in all the areas, Kickstarter made a profit as early as 2010, and successfully for Instagram and WhatsApp provided a lot of famous startups such as seed money. In March 2014, Kickstarter's total amount raised exceeded $ 1 billion. And then, Jingdong raised has not yet launched. Similar contrast abound, here no one by one here.

Nowadays, the United States did not finance companies flocked to the Internet lies in its financial system has been developed under the line, financial services has become a mature, make innovation more difficult. Today the United States ten years ago the United States compared to many financial services and there is no significant difference. While China's underdeveloped financial services, a city infrastructure is complete, Bank outlets across the street, credit cards can also hand several sheets. But other than the first-tier cities are not optimistic, especially in three or four cities, people in the eyes of the "financial" was still went to the Bank to deposit or withdraw money. China has a large number of people not in wealth management services, traditional finance itself did not develop, so there are opportunities for combined with the Internet.

Of course, in the area of electronic commerce and electronic payments in China than the United States started late, but did come from behind. Balance Po also has the potential to do much better than Paypal money market fund. As insurance, chip, Internet banking in the Internet, P2P and other areas, we also catch up with United States trend. But now judge judge which is better or worse, is premature.

United States why there is no "run"?

The past two years, every day, several new domestic companies gain access to Internet banking, and most of these companies have chosen the field of P2P. But at the same time, there is another eye-opening data on average will have less than two days running a P2P platform. People's reactions from the original do not believe, suspicion and shock, anger, human rights defenders, to the now commonplace and completely out of luck. However, in the United States, but there is no similar "run" argument.

On one hand, United States Internet financial company itself is much less than that of China, combined with the monitor very harsh, through supervision of the companies themselves is even more qualified, very few run naturally. In addition, credit national network, can at any time obtain, Americans have attached great importance to their credit. Meanwhile, the default cost is very high, platform did not dare to run. Benefit from the United States a good social credit system, borrowers are also acceptable default rates on the platform, I am investing in you lost is lost.

In China, some of the platform itself is coming for fraud, is ready from the outset to run preparation. After the run, or even change launched a new Web site, continued to cheat, then fled. In addition to the above, there are platforms to win customers, exaggerated, declared at the outset guaranteed, more edge to users in the form of extravagant promises, finally unable to deliver and had to flee.

Co-founder of 91 financial verifications, Tencent technology says in the United States because the FICO credit scoring system is readily available available P2P platforms can clearly determine the credit status of the borrower and borrower credit information disclosed to the lender. For example LC the company itself as an intermediary only charge fees, no risk. At home, in the absence of strong credit data available, so have to take credit for the borrower P2P platform endorsed, this means that the platforms are responsible for the user's funds. Once cannot assume responsibility, only select and run.

Of course, there is also a very important reason is that the regulatory system is not perfect, punishment is not enough, most of the run can go unpunished. And start-up companies in the field of government deregulation of a different, Chinese Internet mainstream companies are calling for tighter regulation of the financial sector, particularly with regard to entry, mainstream companies are called on not to have no professional skills the company has the professional qualification. If a large number of companies with no operational capacity to enter this field, once the economic environment changes, you may experience failures in large quantities or run. But a change in the environment, it will not affect the ability to have a genuine business companies, even good or bad quality were all suspended by regulators is not impossible, it is easy to cause "bad money drives out good money".

No comments:

Post a Comment